.png)

You’ve landed an order of a lifetime, but don’t currently have the financial means as a business to fulfil the order? Don’t stress! A common problem among South African business owners is that they don’t realise they qualify for purchase order funding. In our full guide, we will walk you through everything you need to know so that you don’t bump into any roadblocks or challenges along the way.

What is Purchase Order Funding?

As an SME (Small to Medium Enterprise), you may find yourself in a position where you are unable to fulfil a customer’s purchase order request because you don’t have the materials in stock or the cash to purchase them. When you are faced with cash flow issues like this, your business could risk losing both the order and the customer. That’s where purchase order finance can help.

Purchase order funding (otherwise known as Tender Finance) in South Africa has become a popular way to finance a company that has received a large purchase order from a customer. This is one step before the invoice is generated.

Purchase order finance bridges the gap between order and payment. A purchase order loan is based on the creditworthiness of your buyer (customer) and your business.

Important note: In some ways, purchase order funding is not a loan in the sense that as a business owner you will not receive the funds into your account, it is an advancement on working capital. This means that the funds will be transferred straight to the supplier.

What is a Purchase Order?

A purchase order (also known as a PO) is a document that is used to record the goods or services that a company wants to buy and the price that it will pay for the goods. This official document has a number on it that is used to keep track of the purchasing process.

Who uses purchase orders?

A purchase order is often used when one company wants to buy goods from another company. The buyer will send a purchase order to the seller and ask them to provide all of the details about what they want and how much they are willing to pay for it. Once this information has been received, the seller can then decide whether or not they want to do business with them.

What happens after a purchase order is issued?

It’s important for business owners to remember that a purchase order is (and should always be) a legally binding contract. The moment an organisation accepts a PO, it is legal.

If your buyer refuses to pay for the goods they requested in the PO, as the seller you will be protected by the PO contract. To ensure you are a reputable business, you should also insist that your buyer also have protection in place with a purchase order confirmation. The terms and conditions drawn up in your purchase order should cover any shortfalls on both parties’ sides.

The most important aspect when it comes to requesting funding for POs, is that you have this document as a legal reference.

What industries need purchase order funding?

Any business that received a PO and is facing financial limitations to fulfil the order will need Tender Financing in order to pay suppliers. This type of business loan is designed specifically to help the following industries:

- Retail trade

- Manufacturing

- Import/export

- Wholesalers and distributors

What type of lenders offer purchase order financing?

A long-standing trading history or large amounts of capital – are not always common amongst SMEs – which prohibits them from being able to purchase goods on behalf of their customer. Purchase order funding in South Africa arose when small businesses weren’t given the financial assistance they needed to fulfil orders. The lack of business funding in this sector allowed a gap in the market for alternative lenders. At Funding Hub our lenders review your purchase order and your business’s credit history, rather than just your trading history.

How do I qualify for Purchase Order Funding?

Through FundingHub, you are likely to qualify for Purchase Order Finance if you meet the following criteria:

- Six months trading history

- An average of R40k+ revenue per month

- A contractual Purchase Order

- 20% growth profit margin

* Figures are for example purposes only and may vary from business to business.

How Does Purchase Order Funding Work?

Tender funding has two main features:

- A legitimate purchase order deal – either from the government or a corporate

- Loan approval is based on a combination of the validity of the purchase order as well as the credit history of both the lender and PO customer.

How do I get purchase order funding?

Later on, we will have a look at the 7 steps you’ll need to follow to get purchase order funding. Here is a sneak peek:

How long does Purchase Order funding take?

Once the lenders have approved your funding, they will ensure that the suppliers who help facilitate the purchase order are paid immediately. This is done after the pro forma invoices have been provided. Generally, with our lenders the turnaround time for approval of PO funding is 7-14 days. This depends on a number of factors, but most of the time it has to do with the availability of documents requested by the lender and the time it takes to update the banking details on the customer’s system.

What Can You Use Purchase Order Funding For?

This loan is a bit more specific when it comes to its use. The business loan is granted on the fact that a customer has submitted a purchase order. However, the type of purchase order is of little concern to the lender.

Purchase Order Types

There are mainly two different types of purchase orders:

- Supply and delivery of goods – goods include: electricity, gas, wholesale, printing etc. For these types of purchase orders, the level of experience needed by the borrower will be determined by the lender, in some cases very little experience is required by the lender for the execution of the purchase order.

- Supply of services - services include; construction, installation, manufacturing, facilitation and labour requirements – for this purchase order experience is required, especially in construction, installation and manufacturing.

Remember: Purchase Order Funding is granted because of a purchase order, so you need to prove that the purchase is legally binding from the customer’s side. Meaning they are obligated to pay the invoice once the purchase order has been fulfilled.

PO funding pros & cons

6 Advantages of PO funding

Here are a few reasons why business owners will make use of purchase order finance:

1. It's easy to set up purchase order funding

If you’ve been trading for longer than six months, and have a legit purchase order it’s a whole lot easier to get purchase order financing from alternative lenders than bank financing.

2. Quick set up

If all the necessary guarantees and confirmed POs are in order, purchase order financing allows the process to be expedited with minimal delay. You can access cash or capital quickly from your funders.

3. Purchase orders work with revenue growth

The purchase order financing arrangement can grow alongside your businesses’ expansion. The better and more stable the purchase order, the greater the credit line that can be provided by purchase order funding. The credit line can grow with your revenues

4. Emphasis on your client’s credit history rather than your business

Lenders will rather look at your client’s credit score and history rather than your SME’s. Although in some case’s both the borrower and the client’s credit history will be reviewed, more emphasis is placed on the client for PO funding approval.

5. Your lender will handle the collection

You can take a deep breath. As a business you won’t need to handle any of the debt collection, the lender will be responsible for this. This takes away a lot of the risk for the borrower, as the lender will want to ensure the client repays the loan.

6. Available to new businesses or SMEs

It’s difficult to find a lender that is willing to give a business loan to an unestablished business. Where purchase order funding, allows you to get access to money, granted you are creditworthy and have a proven track record.

7. Free application

FundingHub will never charge you to make an application - or ever. Our service is free, and if you qualify for a purchase order loan in South Africa - we'll help you find it.

5 Disadvantages of PO funding

There are a few cons of purchase order financing too:

1. Finished goods only

This loan will only help companies that supply and deliver finished goods. These goods mustn’t require further manufacturing, assembly, installation, or customization.

2. Direct supplier expenses

The loan is only given for the supplier’s costs and nothing more than that.

3. Minimum gross margins

Most purchase order funding options will only happen if there is a minimum 20% gross margin on the transaction. If the profit margin is notably small, this will make it more difficult to incentivise a funder to provide financing to the supplier.

4. Limitation of workflow process

Purchase order financing is usually given to borrowers who supply a finished product directly to a customer. If you have a longer process you are unlikely to receive purchase order funding support.

5. On-going dependency

This short term solution can elevate expectations for small businesses, and they might require more funding to fulfil ongoing orders. Businesses will need to keep a close eye on managing profits efficiently to avoid this.

How Does the Purchase Order Funding Application Process Work?

Our PO funding application process only takes a few minutes to complete, and we want to make sure we get the right information so you can get the right offer for your needs. In a couple of steps, we can help you secure purchase order funding for your business.

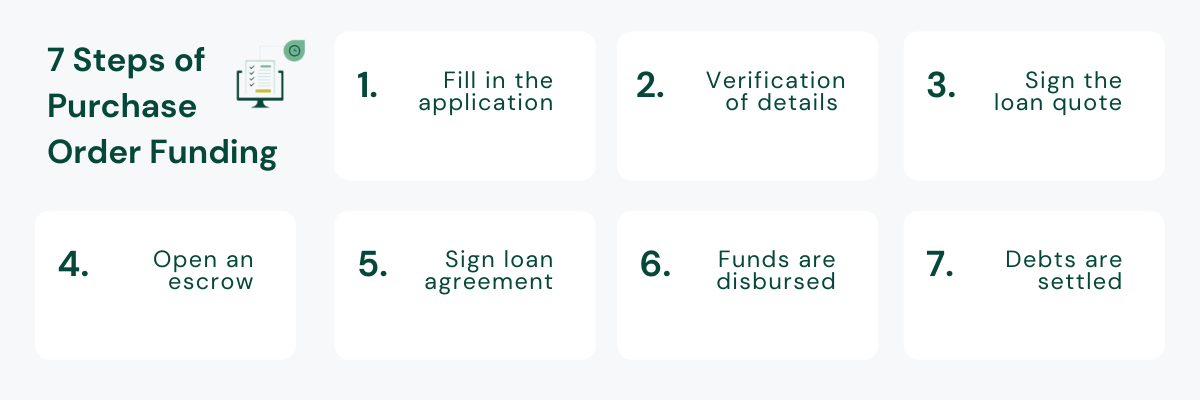

7 steps to get purchase order funding in South Africa

Purchase order lenders will fund the purchase of goods required by the customer on behalf of the awarded business if the following steps are followed:

Step 1 – Start the business funding application

The borrower will start their purchase order funding application process by submitting the following documents:

• Proof of a valid purchase order

• Supplier quotation from a reputable supplier

• CK documents (to prove your company is registered)

• Bank statements or bank confirmation letter

• Identification of all directors

• Any other FICA documents requested by the lender

Step 2 – Verification and vetting

The lender verifies that the order is valid and performs due diligence on the borrower, this includes doing a credit check and making sure that the business’s credit score is up to par. The intensive verification process is a necessary step to avoid any fraud. When the lender is satisfied with all the information collected from the borrower, they will then be sent a detailed cost of the business funding.

Step 3 - Signing the lender quotation

Once the borrower signs the lender’s quote, the lender will secure the transaction by opening an escrow account and ensuring the proceeds of the order go into it.

Step 4 – Opening an escrow account and updating banking details

An approval condition of purchase order financing is that an escrow account will need to be opened, these bank account details will be updated on the customer’s (PO issuer’s) payment system.

Simply put an escrow account (with regards to tender financing) – is a bank account that has been opened under the borrower’s name with all the directors of the business being signatories on the account, including the lender.

An escrow account differs from other joint and ordinary bank accounts because the lender will be the only authorised signatory with transacting powers. The other signatories will have viewing rights only and receive notifications when payments are made into the account. The purpose of the escrow account is for the lender to collect the proceeds of the order that has been funded to settle the borrower’s loan.

Side note - An escrow account is beneficial to the borrower, as the account is under the borrower’s name and may be used for financial statement purposes. Borrowers in the construction space can use statements of escrow accounts to apply for Construction Industry Development Board (CIDB) grading.

Step 5 - Signing the legal agreements

The customer will need to confirm in writing that banking details have been updated to the escrow accounts details (no longer the borrower’s bank details). After this, an agreement will be signed between the lender and borrower, thus bringing the purchase order lending one step closer.

Step 6 – Disbursing funds

In order to reduce the risk of misappropriation of funds by the borrower, the lender will liaise with the supplier. The lender will verify the availability of stock and the banking details of the supplier in order to pay the supplier directly. Once the order has been fulfilled, the goods will then be delivered to the customer along with an invoice which will be submitted by the borrower to the customer.

Step 7 – Settling debts

The customer (PO issuer) will most likely settle the debt 30-60 days from the invoice date, this will be paid straight into the escrow account. The lender will then come along and deduct the loan amount (capital and service fees/ interest), and after which the remaining funds (the profit for the borrower) will be transferred to the borrower’s primary bank account.

Frequently asked questions related to Purchase Order Funding

What’s the difference between inventory funding and purchase order funding?

Inventory funding is a type of financing that offers short-term loans for the purchase of inventory. The borrower receives funds in exchange for their inventory, which they are expected to repay over a specified period of time.

Purchase order financing is the process of providing an organization with working capital in exchange for purchase orders, which are assigned to the lender.

The biggest difference between inventory funding vs purchase order funding is the intent of the funds – one is for inventory the other is for a purchase order.

What’s the difference between purchase order funding and invoice factoring?

Invoice factoring is a type of business loan used when you waiting for invoices to be paid by a client. You’ll request this type of funding when you need a cash injection to tide you over. It’s mostly used when you have already sold the goods or services but the client still needs to pay you.

So the biggest difference here between PO funding and invoice factoring is the time at which the funding is needed during the purchasing cycle. Invoice factoring is needed after you’ve sold the goods or services, where PO funding will be used to secure the purchase order before the goods are delivered or payments are received.

.png)